NPL Analysis: Disputed Payoffs

If you like analyzing loan documents, this article is for you. I use an active lawsuit to show how selecting a default date can materially impact the outcome of an NPL investment.

Extensive litigation is a real risk in NPL investing, especially in judicial foreclosure states. Sometimes litigation cannot be avoided. Some borrowers just enjoy a legal battle. Frequently, the probability of extensive litigation is dependent on the note holder’s level of aggression. For example, a loan default occurs when a payment is missed. The lender elects to accelerate the loan and sells it to an NPL buyer. The NPL buyer reviews the loan file and finds a prior default that occurred over a year ago. They now have a choice: run default interest starting from the payment default date, or run default interest from the prior default event. The former is safer but carries significantly less litigation risk, while the latter is riskier but offers a much larger profit potential.

In this article, I analyze VQ Everglades Investments LLC, VQ Everglades Units LLC, VQ Everglades Buildings LLC, and VQ Everglades Homes LLC v. CNP XXXV Ventures LLC. Case number 2025-020090-CA-01 in Miami-Dade County Circuit Court. VQ accused CNP of inflating the payoffs. As you’ll see, CNP took an aggressive position, which opened the door to the lawsuit.

Background

In September 2014, Biscayne Bank originated 8 loans to VQ Everglades Buildings LLC, VQ Everglades Development LLC, VQ Everglades Investments LLC, VQ Everglades Units LLC, and VQ Everglades Homes LLC. The entities are all controlled by Victor Antonio Quezada Rijo, who also personally guaranteed the loans. The loans are also subject to a Cross-Collateralization and Cross-Default Agreement. In 2019, First-Citizens Bank & Trust Company (FCB) acquired Biscayne Bank. FCB eventually sold the loans to CNP in July 2025.

VQ states FCB sent them a demand letter on May 9, 2025, alleging a loan default due to failure to pay property taxes. VQ did not deny the allegations. They state the default was cured. County records show the property taxes were paid on May 16, 2025.

VQ then states CNP sent them a Notice of Sale and Notice of Acceleration on July 14, 2025. The Notice informed VQ that CNP had acquired the loans from FCB and was accelerating them due to loan defaults. The defaults included failure to pay the property taxes and cure code violations. VQ then requested loan payoffs from CNP. After receiving the loan payoffs, VQ alleges that CNP included fees that are “excessive, duplicative, unauthorized, or unsupported.”

Basically, CNP took an aggressive position on the default interest. They ran default interest from the day the code violations were recorded. VQ disputes that this is allowed. This is the crux of the lawsuit.

VQ’s Argument

VQ makes two arguments:

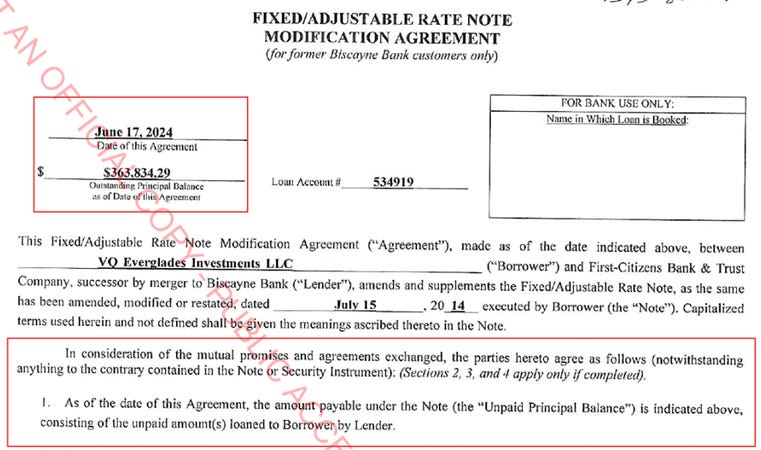

1. VQ and FCB executed Modification Agreements on June 17, 2024. The Modification Agreements fail to mention any default interest or outstanding amounts owed by VQ. Therefore, FCB waived its right to collect default interest before this date

2. VQ cured all the alleged defaults in the demand letter sent by FCB on May 9, 2025.

While there are modifications for each promissory note, the language is the same. For illustrative purposes, I am using loan number 534919 as an example. This is one of the loans in VQ’s lawsuit. Here is the code violation specific to this loan:

CNP is running default interest based on this code violation. What date should they use? The violation date, letter date, or recording date? I don’t know which date they used. If this were a large loan amount, the difference would be hundreds of thousands of dollars. Moreover, the loans have cross-default provisions. CNP could theoretically use a code violation on another property that occurred well before this one.

Onto the Modification Agreement. There are two key sections. VQ will point to page one and argue FCB verified the outstanding amount due as of June 17, 2024. It included just the Principal Balance.

CNP will argue that FCB did not waive any of its rights under the loan documents.

Based on just the Modification Agreements, I don’t think VQ has much of an argument. The lender clearly reserved their rights. However, we need to review the notice provisions in the loan documents. If the loan documents required formal notice, and it was not given, then the lender cannot apply the default interest back to the code violation date. More to come on this.

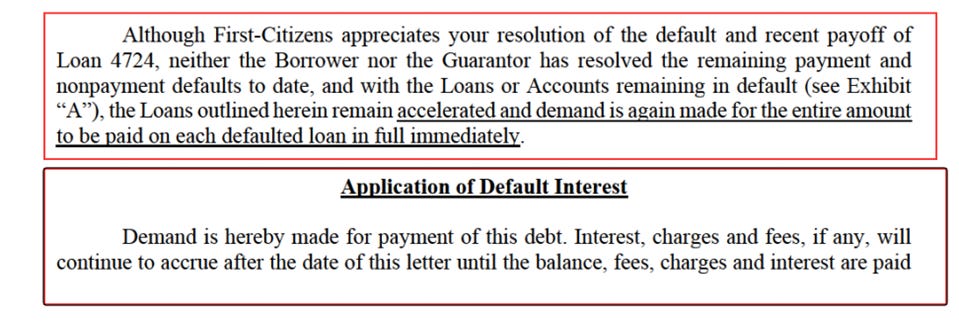

FCB’s demand letter clearly states that there are non-payment defaults, and they need to be cured (i.e., code violations).

FCB confirmed the loan was in default due to payment and non-payment defaults. They gave the borrower 90 days to cure before accelerating the loans. Per County records, the code violation lien specific to loan 534919 was released on July 23, 2025, within the 90 days. However, other code violations remain, and as previously noted, the loans have cross-default provisions.

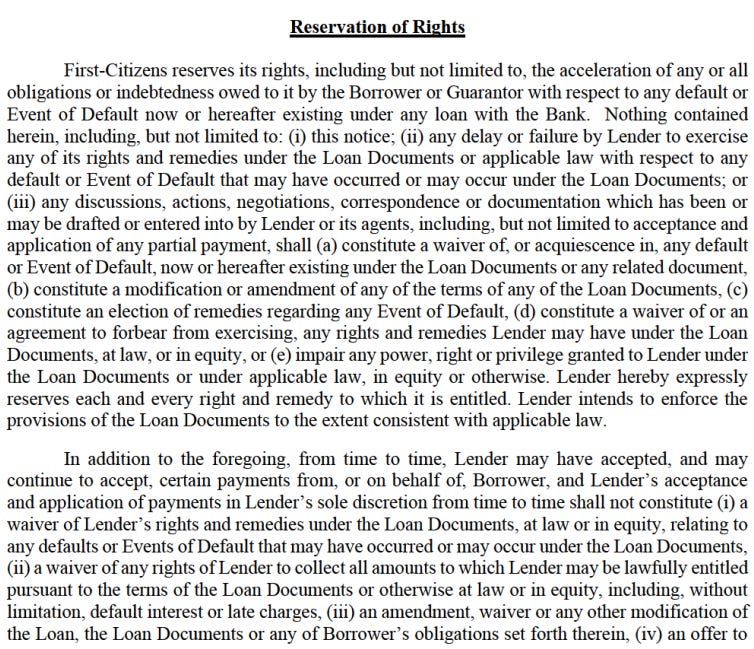

There is one line in the demand letter I would point to if I were VG. “First Citizens is now applying the maximum allowable interest owed to the indebtedness of each Loan, as of May 9, 2025, and thereafter.” This is a decent argument that May 9th is the default date, but CNP can point to the reservation of rights clause in the demand letter:

Loan Documents

Loan 534919 was paid off on July 24, 2025. VQ agreed to pay the amount due but reserved its right to challenge the payoff. CNP recently filed a foreclosure complaint against VQ over the remaining loans. Therefore, we have access to the original loan documents. I had to assume they are the same as loan 534919.

A few notes so no one is confused:

1. Since loan 534919 has been paid off. It is not included in the foreclosure complaint by CNP against VG. Given that the loans were all originated at the same time and the modification agreements contained uniform language, I assumed that the original loan documents for each loan shared the same language.

2. Since there is a Cross-Collateralization and Cross-Default Agreement in place, CNP had to approve the release of the collateral attached to loan 534919. CNP could have declined to release the loan unless all debts were paid in full.

3. If you are a borrower, it is smart to pay off a loan, then challenge the charges. Avoid legal battles when the default interest is running. That being said, if there is insufficient equity, it is not possible.

I reviewed the loan documents. Typically, the loan agreement has detailed language regarding events of default and the corresponding notice provisions. These loan agreements do not have events of default, and the notice section does not discuss a timeline to cure defaults. It only addresses where notices should be sent:

The original promissory notes do contain language regarding default notices, and it is very lender-friendly:

It is clear that formal notice is not required. While the promissory notes do not state the events of default, the mortgages do:

I’m not an attorney or a judge, but based on my review of the loan documents, CNP has the right to apply default interest back to the original loan default. VG really can’t make the case that they were diligently pursuing the cure. The violations were in place for at least a year. In the case of loan 534919, the code violation was cured right before the loan payoff. VG had to clear the code violation to sell the property. They could have cured well before then, but chose not to take action.

Cost-Benefit Analysis

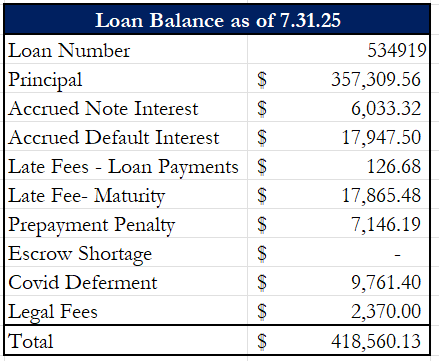

The VQ loans won’t provide a good cost-benefit analysis. Most of the eight loans were under $500,000. In Florida, the max default rate for commercial loans under $500,000 is 18%. For loans over $500,000, the max default rate is 25%. When looking at just loan 534919, the actual default interest is low. Here is CNP’s payoff from their Notice of Sale & Acceleration:

Perhaps CNP didn’t expect pushback, given the actual dollars that are at stake. If litigation is lengthy, the only winners will be the attorneys.

Let’s look at the same timeline, but with a $10 million principal balance. Assume there is plenty of equity in the collateral. The aggressive scenario uses the recording date from the code violation specific to loan 534919 as the default date. The conservative scenario uses FCB’s Notice of Default as the default date.

Assuming a payoff date of October 31, 2025, the difference is $2,328,767 in default interest due.

Is it worth pursuing? With the current loan documents, I think it is. $2.3 million is a substantial amount, and there is a strong chance we will prevail in court. If the loan documents weren’t as strong, I would probably err on the side of caution.

Remember, this analysis is specific to Florida. It may not apply to loans in other states.