Don't Trust. Only Verify.

A little extra due diligence can prevent investment mistakes.

Most of you know me as an NPL buyer, but I’m also active in the private lending world, specifically as a bridge lender in the sub-$20 million loan space. I often refer to it as the Wild West of lending: shady characters, incomplete stories, and questionable financials. Not everyone is like this, far from it. However, I get a deal at least once a week that fits this bill. A little extra due diligence can prevent lenders from making mistakes. Using a lawsuit filed earlier this year, I’ll show how this is done.

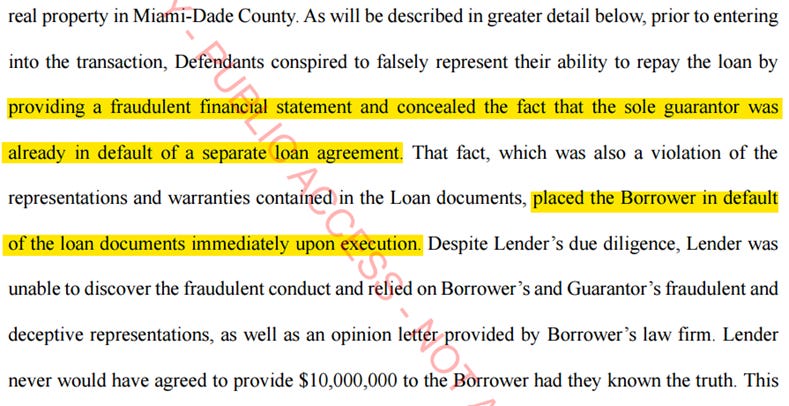

River Tarpon LLC filed a foreclosure complaint against 1515 Miami Development LP in the Miami-Dade County Circuit Court on May 19, 2025. River Tarpon also named the loan guarantor, the debt broker, and the debt brokerage as defendants. River Tarpon accused the defendants of providing false financial statements and of concealing that the sole guarantor was already in default under a separate loan agreement. As a result, the loan was accelerated, and River Tarpon moved to foreclose.

Before reviewing the complaint, it is important to understand the lender, the borrower, the collateral, the transaction history, and the loan structure. I will address it in that order.

Lender

River Tarpon LLC is the lender. The Fiorentino Family Office controls River Tarpon LLC. This is evidenced by the term sheet, which is Exhibit A of the complaint.

Jeffrey Fiorentino signed the term sheet. He also signed the loan documents.

While I do not know Jeffrey, I’ve worked with (and continue to work with) family offices and high-net-worth individuals (HNWI). Real estate lending is typically a small part of their portfolio (if any). Therefore, they tend to lack the experience and expertise required in the Wild West of lending. Again, I do not know Jeffrey. This is just a generalization based on my experience.

Borrower

The borrower is 1515 Miami River Development LP. The address on the loan agreement traces back to Gomez Development Group. The owner, Marlon Gomez, is also one of the guarantors. I am not familiar with Mr. Gomez or his company. Their website claims one successful multifamily development and exit. The other projects appear to be in the pre-construction phase, including the subject property, 1515 Miami River, which is described as 40 townhomes covering 80K SF.

Collateral

The collateral is a ~77K SF development site on the Miami River. It is located at 1515 NW S River Drive, Miami, FL. The property is zoned for multifamily. This area of Miami has attracted developers and continues to grow. Here are pictures from a prior listing:

I assume Gomez Development Group planned for rentals rather than for-sale townhomes.

Transaction History

Per County records, 1515 Miami River Development LP acquired the site from 1515 Miami River LLC in February 2020 for ~$2.2 million.

The managers of 1515 Miami River LLC trace back to Fausto Callava and Antonio Pardo. Both are also named as defendants in the complaint, as they were still involved in the deal.

Since Callava and Pardo were involved in the deal before bringing on Gomez, it is important to look at their transaction history as well. The site has three parcels. All were acquired in 2014, totaling ~$3.9 million. However, the County lists two of the parcel sales as “atypical motivation.” I do not know the story behind their acquisition. The land was refinanced multiple times, starting in 2014, until it was eventually transferred to 1515 Miami River Development LP.

In February 2020, 1515 Miami River Development LP borrowed $4.62 million from Linkvest Capital. I suspect this was structured with an interest reserve.

In May 2022, 1515 Miami River Development LP paid off Linkvest by borrowing $6 million from ROK Lending. Again, I suspect this was structured with an interest reserve. I highly doubt that ROK would provide over $1 million in cash-out proceeds.

Finally, in February 2024, 1515 Miami River Development LP paid off ROK with the loan from River Tarpon LLC, aka The Fiorentino Family Office. As I’ll detail shortly, I know this loan was structured with an interest reserve, as the complaint has exhibits with the loan documents.

While underwriting this loan, the red flags should have been going off:

Land is the riskiest collateral.

The borrower/guarantors likely have little to no cash in the deal at this point.

The borrower likely hasn’t made out-of-pocket loan payments in 4 years.

The loan balance continues to increase due to the borrower’s inability to make payments (i.e., they are rolling interest payments into the loan balance).

The borrower already tapped two of the most active bridge lenders in South Florida: Linkvest and ROK.

Perhaps Fiorentino was interested in developing the site and thought the basis was good. Either they get paid off and earn a high yield, or they foreclose and develop themselves. This is just speculation on my end.

Loan Structure

The complaint did not include the promissory note as an Exhibit, but it did include the term sheet and loan agreement. Based on these documents, here are the terms:

The term sheet references a commitment fee and an exit fee:

The loan agreement has the commitment fee being paid to the broker:

I only bring this up as it affects my sources and uses. I’ll touch on this shortly. I found the interest reserve language in the term sheet interesting. I haven’t seen an exit fee included in a reserve before. This gives a slight increase to the yield. Also, the management fee is essentially a servicing fee. $30K! Another way to slightly increase the yield.

Onto the projected Sources and Uses. Based on the transaction history, I assumed the ROK Lending loan payoff was $6 million. The term sheet and loan agreement provided the brokerage fee and interest reserve. I estimated the closing costs. The stated loan purpose on the term sheet was:

I do not see any reference to a reserve for development plans. I have a hard time believing that the lender would release over $2 million to the borrower at closing. Without a development reserve, that would be the case.

A development reserve would be very beneficial to the lender:

Any progression towards a construction permit should increase the value of the collateral. By holding the funds, the lender controls the process.

By holding a reserve, the actual funds advanced at closing are less. Yet, the lender is charging interest on the full $10 million loan amount. This would further amplify the yield.

FYI: I checked whether the property taxes were paid around the same time as closing. They were not. In fact, the 2024 property taxes are delinquent, and a certificate was issued. This is a monetary default, and the lender failed to include it in their complaint.

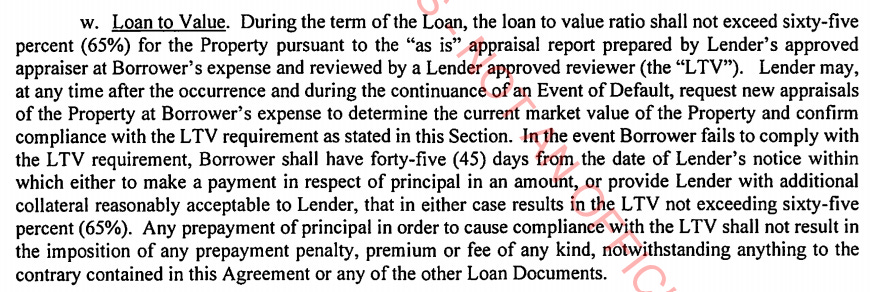

One final note on the loan structure. There is a condition on the term sheet and a covenant in the loan agreement that states the LTV cannot exceed 65%. This is high for a land loan.

Between the transaction history and the loan terms, it seems clear that the borrower had few refinancing options. In fact, this may have been the only one. Between the rate, fees, structure, and costs, the effective borrowing rate was over 20%.

Complaint

The lender cited two issues in the foreclosure complaint:

The borrower/guarantor provided a false financial statement.

The borrower/guarantor failed to disclose that they were in default of another loan.

As a result, the borrower was immediately in default of the loan. Forget 15.50% interest. 25% default interest from day 1!

Before addressing the points, it is important to remember the loan structure. Since the loan had a full term interest reserve, there wouldn’t be any loan payment defaults. Outside of the delinquent property taxes, the earliest monetary default would have been loan maturity.

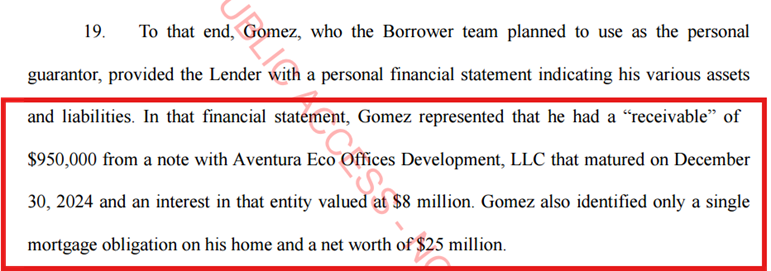

The two issues cited are tied together. According to the complaint, Gomez failed to disclose a mortgage he personally guaranteed, and that the mortgage was in default:

Based on the information presented, it seems clear that the borrower and Gomez misled the lender. Gomez submitted a personal financial statement (PFS) that not only excluded a liability but also failed to disclose that it was in default. As the lender notes, this violated multiple clauses in the loan agreement.

Does the lender have the right to file a complaint? Absolutely. Should the lender be pissed off? Absolutely. Could the lender have flagged this issue and avoided making the loan? Absolutely!

Due diligence requires more than just looking at a PFS. It requires analyzing the PFS and verifying the information. This can be done through additional documentation requests or public records. For example, if you want to verify a guarantor’s liquidity, you request a bank statement. If you wish to confirm a guarantor’s real estate holdings, you use public records.

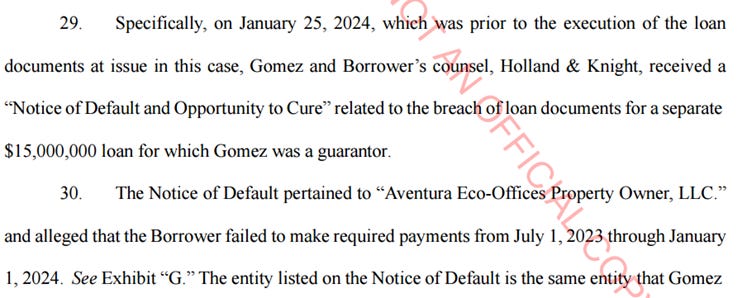

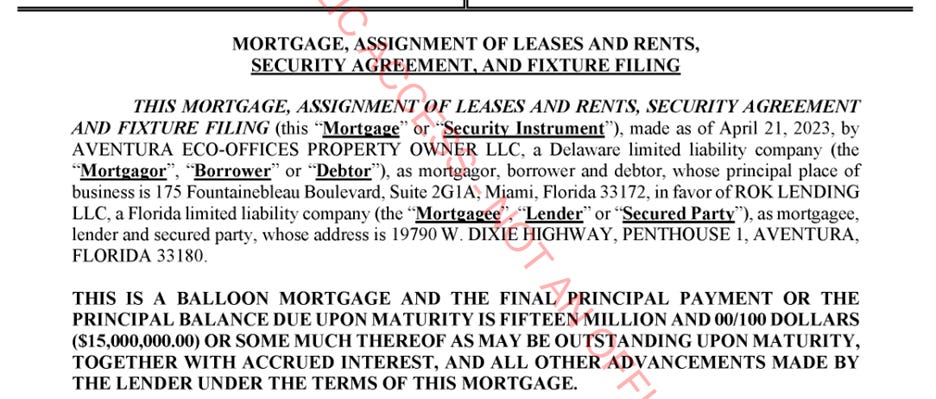

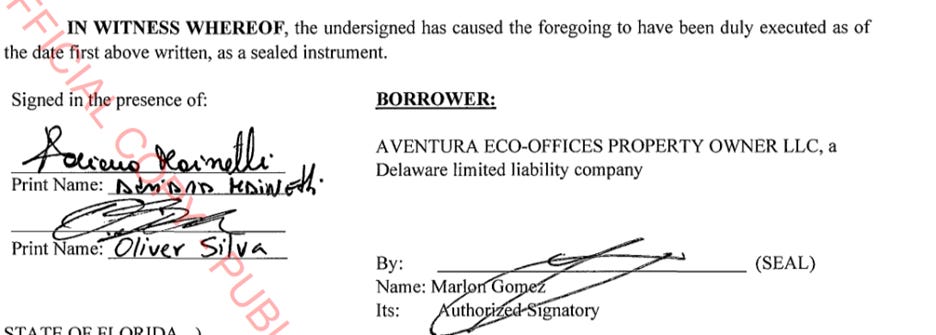

Looking into Aventura Eco-Offices Property Owner LLC would have taken less than 5 minutes. After all, the lender is claiming it was critical to the loan approval, as Gomez claimed a $950,000 receivable, $8 million in equity, and no mortgage liability.

I pulled the recorded mortgage. Aventura Eco-Offices Property Owner LLC borrowed $15 million from ROK Lending. Yes, the same ROK that the lender would pay off on this transaction. Furthermore, Gomez signed the mortgage.

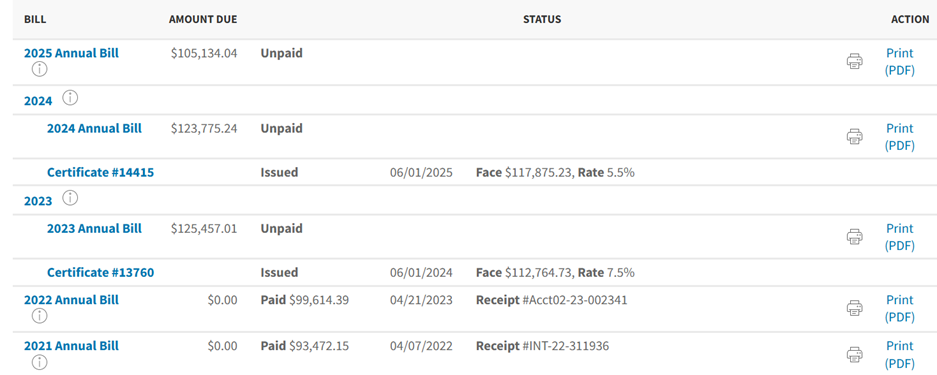

If you have experience lending money in South Florida, you know the probability that this is a nonrecourse loan is almost zero. Additionally, I checked the property's taxes. They haven’t been paid since 2022. Even then, they were late!

Again, this whole process didn’t take long. The lender should have checked. It doesn’t excuse the borrower’s behavior. The lender has every right to go after them. But the lender could have avoided a bad decision. Now they are tied up in litigation, and I question if the true value of the collateral is even above the loan amount.

Public records are your friend. In my opinion, Florida has the best public record system. Almost every county has user-friendly databases. Use them to your advantage. It has prevented me from making mistakes in the past, and it will continue to do so in the future.

As a side note, ROK Lending foreclosed on Aventura Eco-Offices Property Owner LLC and took title to the property (also a development site). River Tarpon LLC will eventually foreclose on 1515 Miami Development LP.

Any questions? Feel free to reach out.

I love reading your stuff, thanks for writing!!

The more I read, the clearer it becomes to me that you should be teaching brokers!!! Your stuff is gold.... So glad I have access to you...